shipping decarbonization concept

shipping decarbonization concept

Shipping must align with the Paris Agreement temperature goal and be run entirely on net-zero energy sources by 2050. Over 200 signatories to the industry-led Call to Action to decarbonize shipping firmly believe that urgent and equitable decarbonization of the maritime supply chain by 2050 is possible and necessary.

The private sector is leading the way and taking concrete actions to make zero-emission vessels and fuels the default choice by 2030. Decisive government action and enabling policy frameworks are needed to reach our 2030 and 2050 ambitions.

As the shipping industry navigates the transition from fossil fuels to zero-emission fuels, they are exposed to risks and uncertainties. The Getting to Zero Coalition has identified three key factors to making better-informed investment decisions: tracking the hydrogen economy; incorporating the total cost of operation; and investing in optionality and flexibility.

1. Tracking the hydrogen economy

As the shipping industry explores what the scalable zero-emission fuels of the future will be, there is broad acknowledgement that hydrogen-based fuels with zero or net-zero carbon will play a critical role in the medium and long term.

• While hydrogen’s low energy density does not allow it to be a fuel for deep-sea shipping, it can be part of a flexible pathway to fully decarbonize the maritime industry, as it is a feedstock for zero-emission ammonia and methanol — leading candidates to enable the transition to zero by mid-century. It could also be used for other synthetic hydrocarbons such as methane.

• Globally, around 500 million to 800 million tons of zero-emission hydrogen is needed to produce green or blue ammonia and methanol by mid-century. It is four to six times higher than today’s need. While 70 percent will be provided by direct electricity, hydrogen (and its derivative) will account for 15-20 percent of world final energy demand.

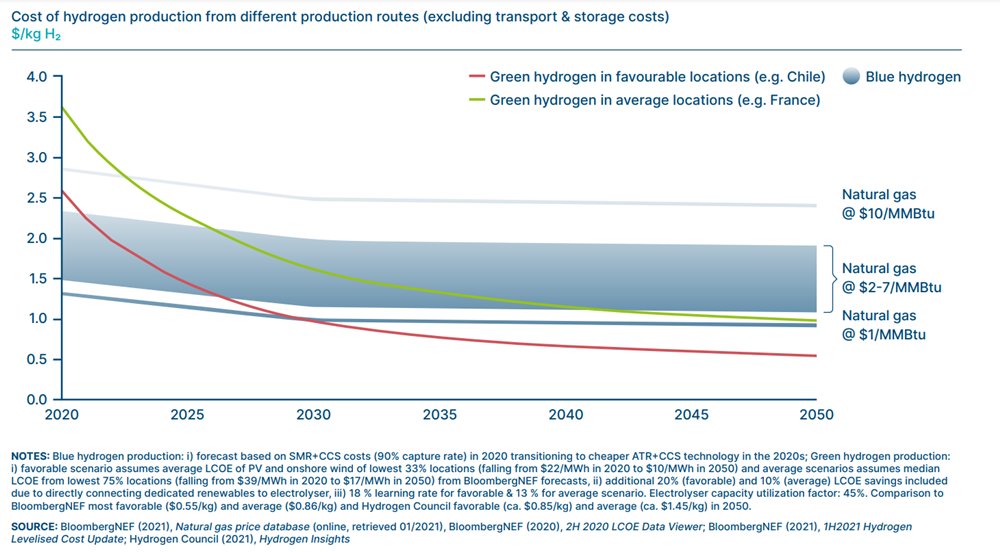

• About 95 percent of the world’s hydrogen comes from fossil fuels. In the near to medium-term, the cheapest green hydrogen will come from countries such as Chile, which has cheap solar production costs. Green hydrogen is produced via electrolysis of water using renewable electricity such as wind and solar power (see Figure 1 below).

• Supply chain costs will vary depending on the form in which hydrogen will be transported by pipeline, truck or ship. Transporting hydrogen by sea requires conversion into a more energy-dense carrier such as ammonia, although efficiency losses must be accounted for. The optimal hydrogen transport mode will vary by distance, terrain and end-use: no universal solution exists.

2. Considering the total cost of operation

The total cost of operation (TCO) is the purchase price of an asset plus the costs associated with its operation, use and disposal over its lifetime. To calculate it, a techno-economic model is the best tool. Indeed, it is a simplified depiction of reality, designed to aid decision-making and, eventually, investments.

• In order to calculate TCO, modeling is used as a tool. The input, outputs, assumptions and sensitivity analysis when modeling aim at reducing uncertainties to identify key drivers and test hypotheses.

• Model outcomes help to accelerate decision making on the transition pathway, provide evidence for research, development and deployment (RD&D) investments, and support pilots that contribute to scaled solutions.

• As renewable energy costs are decreasing, zero-emissions fuel competitiveness will improve over time due to decreasing production costs. Lloyds Register and UMAS have shown expected increases of the TCO for vessels powered by Heavy Fuel Oil (HFO) and Low Sulfur Fuel Oil (LFSO).

• Policy and regulation will play a major role in overcoming high costs of scaleable zero-emission fuels, while 87 percent of the estimated $1.4 trillion-1.9 trillion investment needed for future shipping fuels will be onshore

3. Understanding optionality and flexibility

To mitigate business risks associated with fuel-related uncertainties, it is fundamental to invest in fuel flexible solutions. In the near future, dual fuel two-stroke engines can respond to the needs of new design and retrofitting.

• As there is no single future fuel, dual fuels engines, optionality for onboard fuel storage, flexibility in technologies, and retrofit readiness are key factors to successfully transition.

• Booking the first orders and aligning supply and demand are key drivers to accelerate the commercialization and deployment of next-generation engines. A recent study conducted by the University of Maritime Advisory Services (UMAS) and the Getting to Zero Coalition indicates that by 2046 the number of retrofits will reach around 35,000 vessels — nearly half the global fleet (see Figure 2 below).

Figure 2: Amount of newbuilding and retrofitting to zero-emission fuels. Source: UMAS and Getting to Zero Coalition (2021). decarbonize shipping

Figure 2: Amount of newbuilding and retrofitting to zero-emission fuels. Source: UMAS and Getting to Zero Coalition (2021). decarbonize shipping

• Retrofitting offers the possibility to remain flexible on the transition pathway. Indeed, it is an opportunity to tailor the vessels to meet global standards and adapt to fuel availability.

• Due to differences in energy density between fuels, bunkering, onboard systems and storage must be considered in the design stage. This is true whether vessels are new or retrofitted. Ammonia, methanol and methane are viable deep-sea shipping fuels, while compressed and liquid hydrogen are not (see Figure 3 below).

• To accelerate the retrofitting process, there is a need to develop a common understanding on retrofit readiness and engage stakeholders across the value chain, including shipowners, shipyards and shipping banks.

Figure 3. Ammonia, methanol and methane are viable deep sea shipping fuels, while compressed and liquid hydrogen are not.

Figure 3. Ammonia, methanol and methane are viable deep sea shipping fuels, while compressed and liquid hydrogen are not.

The Getting to Zero Coalition will continue to explore zero-emission fuel optionality in 2022, including a deeper dive into fuel optionality pathways and a forward-looking analysis of newbuild and retrofit vessel options — starting from the existing range of vessel configurations. The objective of this ongoing work is to allow shipowners and financiers to accelerate zero-emission investments by considering possible pathways to zero-emission shipping must be incorporated into all investment decisions from today.