Image credit: 123rf

Image credit: 123rf

Southeast Asia is experiencing unprecedented fuel price increases and volatility, increasing demand for power, and exposure to the intensifying impacts of climate change, writes Frederic Carron, Vice President Middle East Asia, Energy Business at Wärtsilä.

However, amidst this uncertainty, leaders have the opportunity of a generation – to transform their power systems so that they are optimised, sustainable and scalable for the future.

In order to realise a net zero future, there are realities to be faced. Inflexible fossil fuel power plants need to be phased out, while renewable energy capacity and flexible power solutions must be built in. Clean energy supply chains need to be scaled up and sound policy frameworks must be communicated and implemented by policymakers to support the uptake of clean energy systems.

By front-loading the deployment of renewables now, Southeast Asian countries can accelerate decarbonisation. What’s more, those systems do not need to cost more and could allow the countries to avoid future carbon taxes and the threat of stranded assets.

A window into Southeast Asia’s future

Southeast Asia is rapidly emerging as a colossus of the global economy, with nearly all of its economies more than doubling in size since 2000. This growth has largely been powered by fossil fuels.

Across the region, the annual average fossil fuel import bill has been $43 billion USD or 1.7% of GDP over the past decade. However, based on current commodity prices, these costs are set to significantly increase. The International Energy Agency (IEA) forecasts that fuel imports and energy security vulnerabilities will rise sharply in Southeast Asia unless clear planning and bold action is taken to accelerate the energy transition towards renewables.

At the same time, net zero commitments are proliferating worldwide, encompassing 91% of global GDP. Science-aligned net zero pathways are now the baseline expectation for countries, companies, cities and regions. Having a clear, actionable roadmap to net zero is fast becoming a prerequisite for international trade. Massive opportunities are on the table for countries that can get ahead of the net zero wave; the World Bank estimates that the Asia-Pacific region can create $47 trillion USD of growth by 2070 through transitions to net zero. The planned ASEAN Power Grid is one example, where the development of a power trading network for renewables will help the region to meet rising regional and global demand for green power.

Southeast Asia is on the front line of the intensifying impacts of climate change. In my view, it is now vital that national-level net zero pledges and decarbonisation goals are operationalised across the region’s economies.

Pioneering change in the power sector

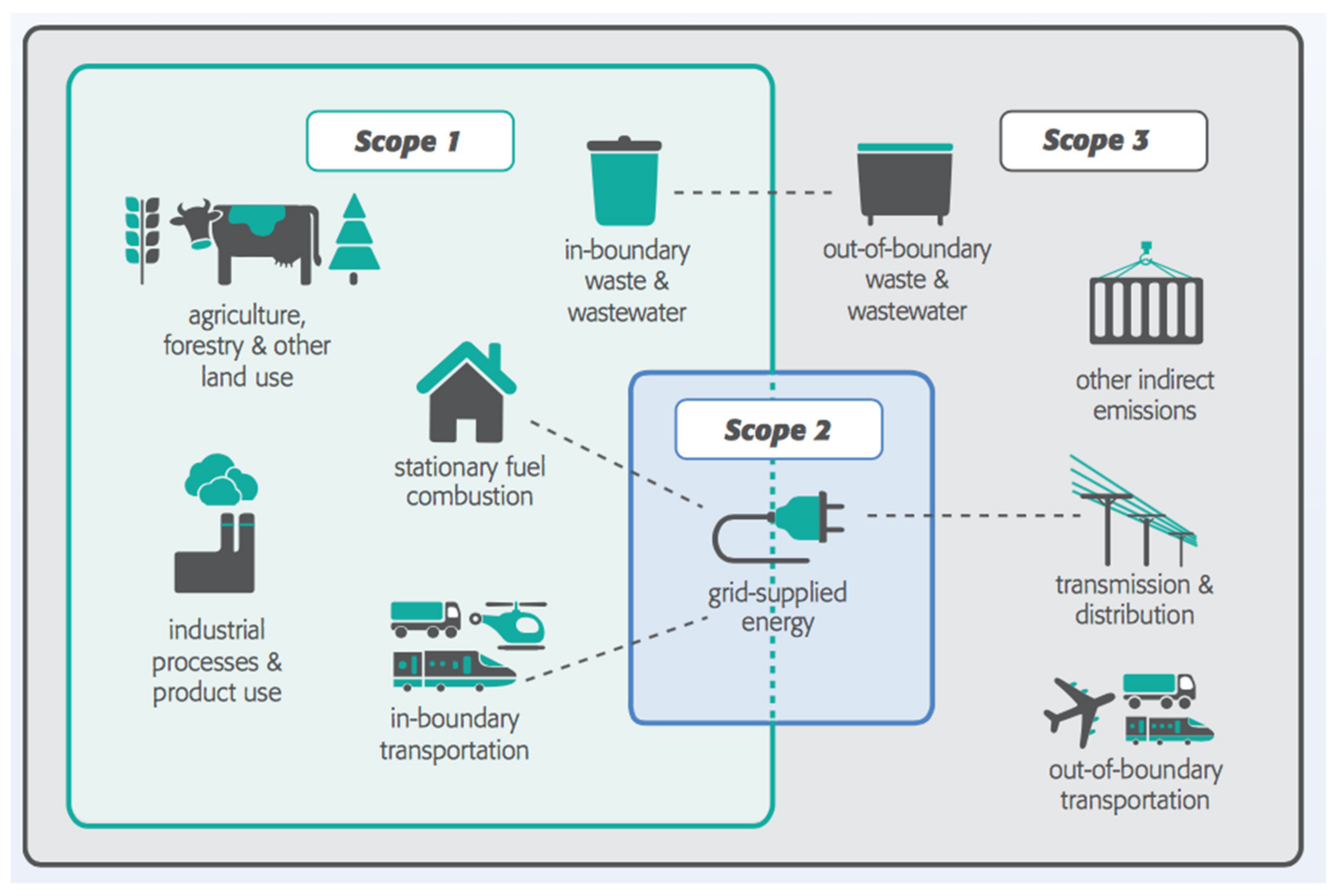

In 2020, 40% of Southeast Asia’s emissions came from power generation, followed by industry (29%) and road transport (18%). Power sector leaders hold the keys to pioneering decarbonisation of the region’s economies. All the technologies needed to decarbonise power exist commercially today, and Southeast Asia benefits from a diverse range of renewable resources, including hydropower, wind, solar PV, bioenergy and geothermal.

Progress is already being made. Renewables account for nearly a quarter of total generation in Southeast Asia, with the majority coming from hydropower, and the region aspires to achieve a 35% share of renewable electricity capacity by 2025. However, in our experience of modelling power systems around the world, a far higher share of renewables can reliably meet rising demand for power this decade, while dramatically cutting emissions.

To demonstrate the potential in Southeast Asia, Wärtsilä has modelled power systems in Vietnam, the Philippines and Indonesia in the Rethinking Energy in Southeast Asia report. The results are striking. Building flexible renewable-based power systems in these countries can be more cost-effective than running traditional systems that continue to rely on fossil fuels. As the modelling has shown in other regions around the world, shifting from fossil fuels to renewable energy significantly reduces a power system’s operational expenditure. This is because a flexible renewable grid requires minimal levels of balancing fuel and low maintenance. In fact, by reaching net zero, when factoring in the carbon taxes forecasted by the IEA, the levelised cost of electricity (LCOE) of net zero power systems in these three countries can be up to 23% lower than a system that continues to rely on inflexible fossil fuel for baseload power.

Flexibility, the best friend of renewables

To achieve a level of 85% renewables in 2050, which would align with the Paris Agreement, the IEA forecasts that Southeast Asia must collectively deploy 1,100 GW of renewable capacity in the next 30 years – this is equivalent to the combined total renewable capacity of China and India today.

However, the coal power plants and large combined cycle gas turbines (CCGTs) that currently dominate power systems in Southeast Asia cannot adapt to the intermittent nature of renewables, forcing some countries to curtail massive amounts of clean energy. For renewable energy to become the main source of energy, grids must be equipped to balance, store and optimise renewable energy.

Flexible capacity, provided by balancing engines and energy storage, creates the conditions where renewables are the most cost-efficient way to power our grids: by balancing intermittency and ensuring backup power is available when there is insufficient wind or solar. In my view, the systemic wastage of power caused by the inflexibility of legacy infrastructure needs to be urgently addressed by Southeast Asia’s governments and regulators for the lowest cost energy source, renewable power, to fulfil its potential.

Understanding the interplay between short and long term

Shifting away from Southeast Asia’s current fossil-dependent system demands an unprecedented transformation in power sector strategies, power plant portfolios, and operations. Policymakers must play their role by shaping new markets and recognising the systemic cost of inflexibility, which is often hidden or spread across fossil fuel portfolios.

Through Wärtsilä’s power systems modelling of Southeast Asian countries, including the Philippines, Vietnam and Indonesia, we know it is possible for them to fully utilise renewable resources and unlock net zero power systems at the lowest cost and risk, and maximum reliability and affordability.

In doing so, Southeast Asia has an opportunity. As it emerges as a powerhouse of the global economy, renewable energy can deliver cheaper and more reliable electricity. However, pivoting from baseload fossil fuel to a flexible renewable system is a complex, multi-year project. This transition must begin today if its full benefits are to be unlocked and targets to be achieved.