DNV, the independent energy expert and assurance provider, has published new research about the industry’s perception of the growing market for floating offshore wind and its possibilities for mass commercialization.

The research, which surveyed 244 developers, investors, manufacturers, advisors and operators across the globe, found that 60% of respondents think floating offshore wind will reach full commercialization by 2035, with 25% believing it will be as early as 2030.

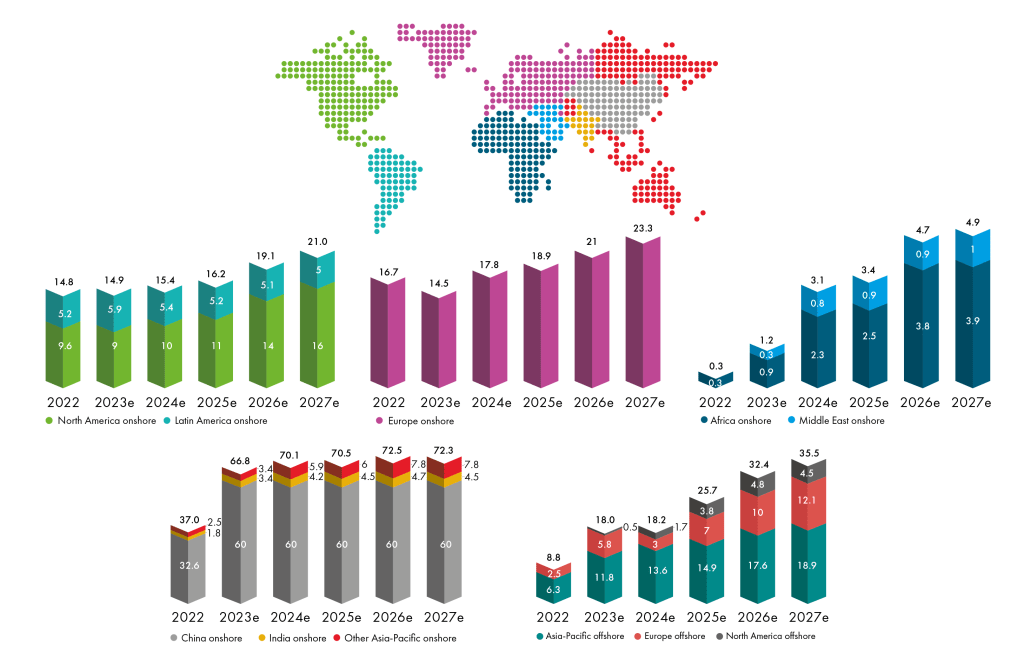

Reaching these targets is ambitious, but early signs are promising, with 60% of organizations with revenue-producing business in wind expecting to increase investment in floating offshore wind in 2023.

“The view from the industry is clear. There is overwhelming confidence that floating wind can achieve commercial success in a little over 10 years. DNV predicts that by 2050, 15% of all offshore wind installed capacity will come from floating turbines. However, barriers must be overcome. Governments can play a leading role in making the market attractive for investment, with long-term, stable policy and regulatory frameworks, and by adapting critical infrastructure such as grids and ports. The industry itself will need to look at cost reduction through greater standardization and scale-up. As DNV we are committed to supporting the industry. This is an exciting time for the industry, as we move towards commercialization, floating offshore wind is opening new possibilities for wind power locations and will play a critical role in the transition to a cleaner energy supply,” comments Ditlev Engel, CEO, Energy Systems at DNV.

Reaching full commercialization will depend, in part, on the investment potential of key markets. Market size was cited by 21% of respondents as the first criteria for choosing a market to invest in, followed by regulatory and political stability (16%), and power grid suitability (12%).

For floating offshore wind to scale-up, it is paramount that its levelized cost of energy (LCOE) drops as much and as quickly as possible. DNV’s Energy Transition Outlook forecasts that levelized costs for floating offshore wind will fall by almost 80% by 2050. 21% of survey respondents believe that standardization – either through a reduction in the number of concepts or the emergence of a preferable concept will be the biggest factor for LCOE reduction. Bigger turbines and industrialization come next, closely followed by larger wind farms (allowing for economies of scale and greater installed capacity). Standardization was also cited by the industry as a crucial factor to mitigate risk.

Supply-chain challenges also come into play, as the offshore wind sector is battling high commodity prices and capacity limitations. The top risk cited by floating wind professionals was a lack of port infrastructure.

The second biggest risk cited was installation vessel availability, tied with capacity. While floating wind is generally not reliant on the advanced and bespoke vessels used in bottom-fixed offshore wind, the sheer number of mooring and anchoring installation vessels and the capabilities required could be a challenge for the industry, as more moorings and anchors are set to be installed over the next 10 years than have ever been seen in the oil and gas industry.

“Commercial attractiveness will rely on cost reduction and capture prices in various markets. Cost reduction does not happen by waiting, which makes it crucial that the first generation of larger floating windfarms are installed by 2030, to deliver on the promising outlook for floating wind,” explains Magnus Ebbesen, Segment Lead Floating Offshore Wind at DNV.

About 300 GW of floating offshore wind will be installed globally in the next 30 years, requiring around 20,000 turbines, each mounted on top of floating structures weighing more than 5,000 tonnes and secured with so many mooring lines that if they were tied end-to-end, they would wrap around the world twice.