Renewable energy auctions in Europe are experiencing two contrasting trends. While the offshore wind segment has witnessed intense competition resulting in subsidy-free bids across major countries, the renewable power auctions have been undersubscribed in the past year due to several factors such as increased raw material costs, rising logistics expenses, higher interest rates, and prolonged approval procedures. As a result, there is a need to address the underlying challenges to ensure the sustainable growth of the renewable energy sector, says GlobalData a leading data and analytics company.

GlobalData’s latest report, “Europe Renewable Energy Policy Handbook 2023, Update,” notes that zero-subsidy bids are gaining traction. For instance, in December 2021, RWE won a zero-subsidy tender for the 1GW thor offshore wind project in Denmark. A similar trend was witnessed in Germany, as a 658MW project in the North Sea and 300MW site in the Baltic Sea both closed at zero-subsidy bids. The latest auction concluded in Germany in September 2022 for a 980MW project in the North Sea was also won by RWE, at a zero-subsidy bid.

Attaurrahman Ojindaram Saibasan, Power Analyst at GlobalData, comments: “Advancements in technology and the estimated costs of producing electricity during the commissioning of offshore wind power plants have enabled them to confidently let go off government subsidies.”

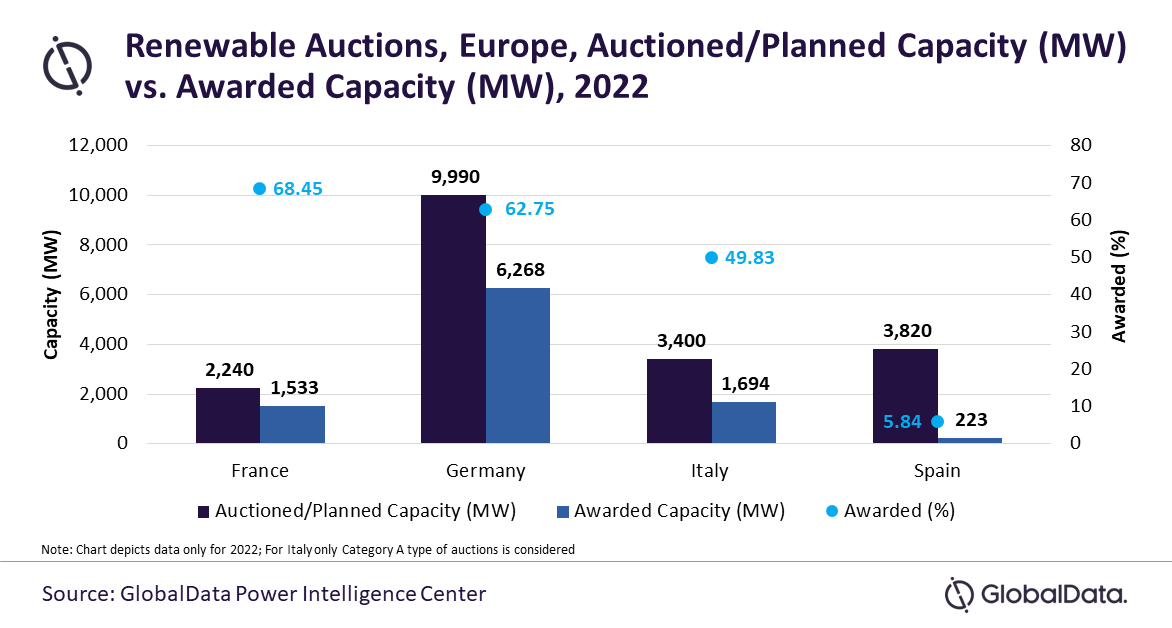

In October 2021, the Danish Energy Agency (DEA) announced that not a single bid was received for the technology neutral tender in June 2021. A similar scenario was witnessed among other major European nations in 2022. It was an underwhelming year for German solar PV auctions, with both ground-mounted and rooftop auctions underperforming. A total of 4,858MW capacity was offered, of which only 2,897MW were subscribed.

In Italy, of the total 10 rounds of renewable energy auctions conducted for Category A, only the first auction’s planned capacity was fully allocated. Between 2019 and 2022, a total of 7.3GW planned auctions were conducted, of which only 3.9GW of projects were awarded which is a little over half of the capacity offered.

Spain introduced updated auctions in 2021, which initially received a tremendous response, with both auctions conducted that year being oversubscribed. In 2022, the two rounds of auctions were a failure, with only 223MW capacity awarded in the year against the auctioned capacity of 3,820MW.

Similarly, in France, the auction program underperformed between 2018 and 2022 due to the low ceiling price set by the government and additional scrutiny of bid applications. However, the last solar PV self-consumption round conducted in 2022 received an overwhelming response, with the awarded capacity exceeding the auctioned capacity, which is a positive for the French renewable auctions in 2023.

The low ceiling price of auctions has also been a major reason. The developers are unable to bid at a lower price due to the rising cost of equipment and components across the value chain. The developers in the region face several challenges, such as rising inflation, supply chain constraints, high raw material costs, and an increase in logistics expenses. Moreover, schemes like the secret price mechanism launched by Spain have not been well received among the industry participants.

Saibasan concludes: “The European governments should look at increasing support by raising the ceiling price and reducing the time for approval processes. They may also consider the contracts for difference scheme which will reduce the burden on the government by paying only the differential price as well as benefit the developers by protecting them from fluctuating energy costs.”