Yole Group is forecasting a $100-billion automotive semiconductor market in 2029, with the semiconductor device value per car rising to about $1,000 from around $590 per car in 2023.

The most invested automotive semiconductor segments by OEM are power electronics, high-performance SoCs for ADAS, cockpit and MCUs for future E/E architectures.

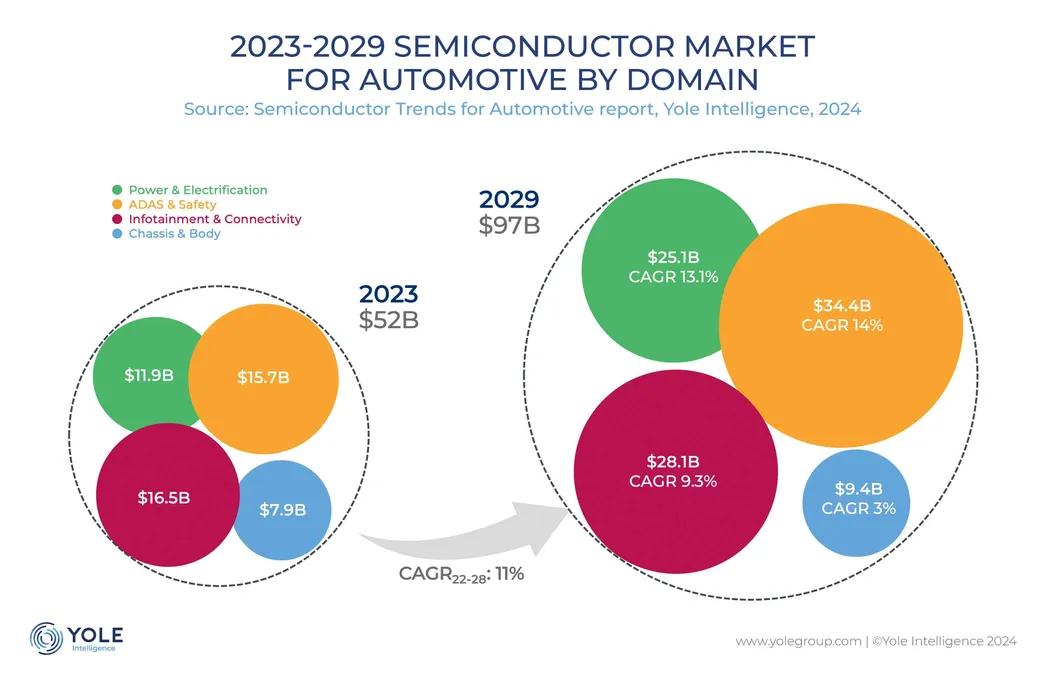

ADAS and safety will experience the highest growth with 14% CAGR between 2023 and 2029. Electrification is not included, as it is the second-largest market driver for semiconductor growth with more than 13% CAGR during the same period. And even though electrification in Europe is slowing down compared to last year, the Chinese market is still highly active in that field.

Yole has expanded its ‘Triple-C’ model—a specialized tool designed to help OEMs develop their individual semiconductor strategies—to include all of the top 20 global OEM groups, along with leading Chinese EV startups such as Nio, XPeng, and Li Auto. The 2024 analysis highlights significant diversity within the ecosystem.

On average, OEMs are becoming more deeply engaged in the semiconductor sector. Another notable trend is that Chinese OEMs are making broader investments in various types of chips and are more deeply involved in the upstream supply chain. Power modules, which are critical enablers for EVs, serve as a prime example. Nearly all Chinese OEMs have investments in this segment across various formats. In addition to power modules, high-performance processors and MCUs are also highly favored by OEMs.