According to InfoLink’s global lithium-ion battery supply chain database, energy storage cell shipments reached 202.3 GWh in the first three quarters of 2024, up 42.8% YoY. The energy storage cell market experienced robust sequential growth during the first three quarters, with shipments in Q3 rising by 16% QoQ, setting a record high for single-quarter shipments.

Competition among top 10 manufacturers intensified amid high industry concentration

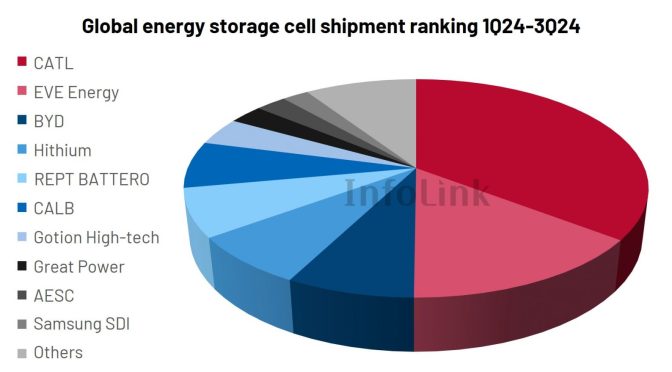

Industry concentration remained high in the first three quarters of 2024, with a CR10 of 90.7%, staying at historically elevated levels, consistent with the first half. The top five largest energy storage cell manufacturers in the first three quarters were CATL, EVE Energy, BYD, Hithium, and REPT BATTERO.

Key market themes for Q4: stabilization, intensification, rises, downturns, and emergence.

Stabilization: CATL maintained its top position as the global leader, leveraging its robust global operational capabilities. Thanks to major clients like HyperStrong and Powin, EVE Energy continued to expand its market share and secured its position as the second-largest player in the industry.

Intensification: The competition among the third to sixth-ranked players—BYD, Hithium, REPT, and CALB—remains fierce, with a market share gap of less than 1%.

Rises: BYD’s shipments to the Americas have gradually increased, underpinning overall shipments, with its ranking rising to third place. Great Power’s significant boost in residential storage shipments has propelled its ranking to eighth.

Downturns: Given the excellent performance of Chinese manufacturers, the market share of South Korean peers has been squeezed. SDI and LG rank tenth and eleventh in the industry, with their combined market share dropping. Moving forward, the transition from NCM/NCA to LFP must be accelerated, and efforts to enhance order acquisition in the Americas should be intensified to address market competition.

Emergence: InfoLink continues to monitor manufacturers outside the top ten, with some, such as Sunwoda, showing substantial shipment growth in the third quarter. InfoLink will keep tracking their further collaborations with major clients.

241115_InfoLink_Global battery shipment ranking 3Q24_en_1

*Source: InfoLink’s Global lithium-ion battery supply chain database

*InfoLink strives for information comprehensiveness, but in case of any discrepancies with official data, manufacturers’ official data shall prevail.

Strong growth in utility-scale energy storage; market share of 300Ah+ cells continues to grow

In the first three quarters of 2024, global utility-scale energy storage cell shipments reached 180 GWh, up 49.4% YoY. The top five manufacturers, CATL, EVE Energy, Hithium, CALB, and BYD, dominate the market, with the top two holding nearly 55% combined share. Hithium, CALB, and BYD each shipped over 10 GWh with similar volumes.

300Ah+ cells accounted for almost 40% of the market share in Q3, while interest in 500Ah+ cells is rising, with leading manufacturers making plans for mass production. However, 300Ah+ cells may remain the market standard for 2024–2025, as 500Ah+ products still need time for validation.

*InfoLink strives for information comprehensiveness, but in case of any discrepancies with official data, manufacturers’ official data shall prevail.

Small-scale storage recovers with broader demand

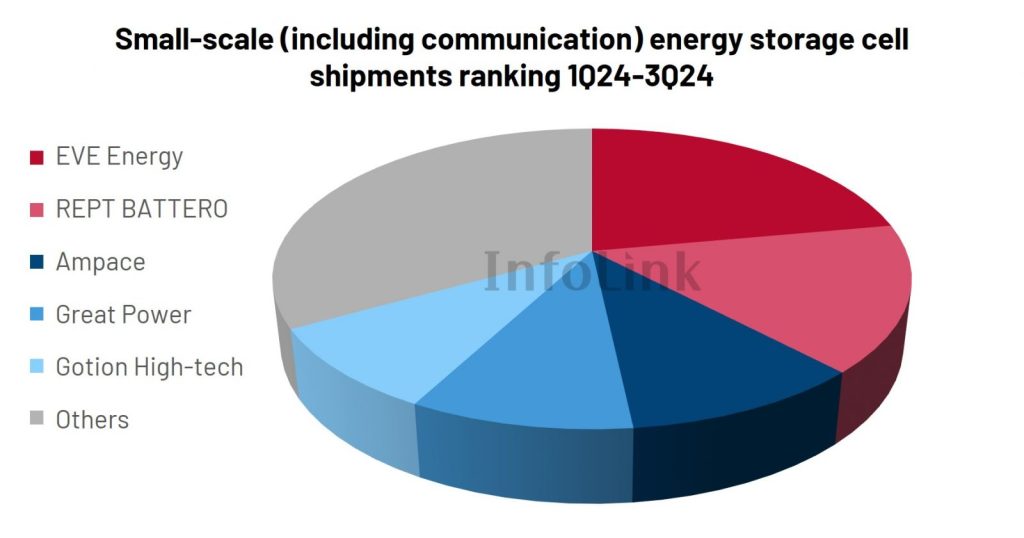

In the first three quarters of 2024, global small-scale energy storage cell shipments reached 22.3 GWh, up 5.2% YoY. shipments in Q3 grew 12.9% QoQ, signaling continued recovery. The top five companies were EVE Energy, REPT, Ampace, Great Power, and Gotion High-tech. Competition remains fierce, and industry concentration keeps falling, with CR5 dropping below 70%. EVE Energy and REPT lead the market, ranking first and second in the industry, while the market share gap between the third to fifth places remain small.

The residential-focused market is becoming less reliant on Europe and America, with demand expanding to Asia, Africa, and Latin America. This shift requires manufacturers to broaden their coverage and partner with customers who have strong global reach and foresight.

*InfoLink strives for information comprehensiveness, but in case of any discrepancies with official data, manufacturers’ official data shall prevail.

This quarter, the share of overseas shipments from several Chinese manufacturers has increased, marking progress in international expansion. However, rising policy risks abroad call for strategies to build a strong “second stronghold overseas.”

InfoLink encourages resilience with the message: “Stay diligent and vigilant to succeed despite challenges,” hoping that manufacturers can navigate challenges and rise against the trend.